So, you want to know the meaning and definition of “Person” u/s 2(31) of the Income Tax Act 1961?

You are in the right place.

Here you will get every information about the term “Person” u/s 2(31).

So, let’s start our discussion.

Contents

Definition of Person u/s 2(31) of the Income Tax Act 1961

The term “Person” includes:

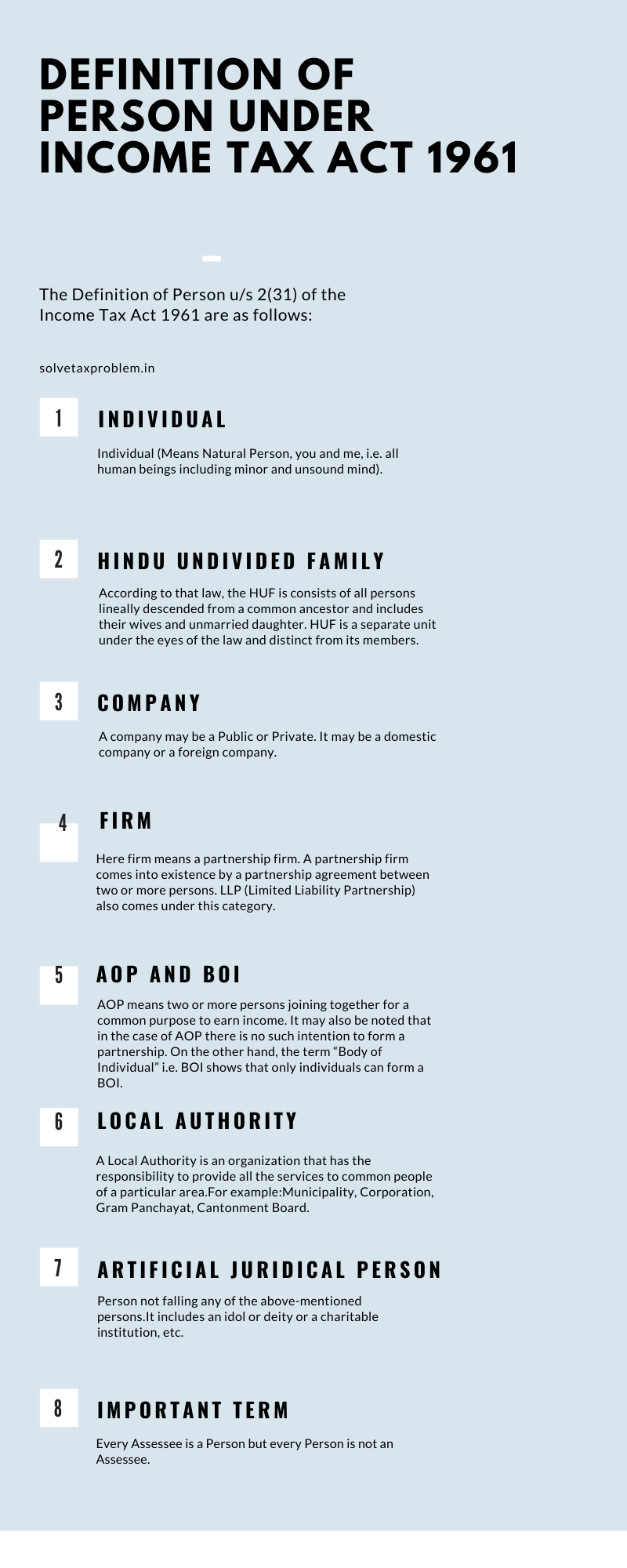

- Individual (Means Natural Person, you and me, i.e. all human beings including minor and unsound mind).

- HUF,

- Company,

- Firm,

- Association of Persons (AOP) or Body of Individuals, whether incorporated or not,

- Local Authority, and

- Artificial Juridical Person

It is a proper definition as given by the Income Tax Act 1961.

Now all the above-mentioned terms are explained below.

Individual

Here individual means all human beings.

It may be anybody. Just like you and me.

It may also be noted that the term “Person” includes a minor or an unsound mind.

No matter you are a minor or an unsound mind if you have a taxable income you have to pay the tax.

However, in the case of a minor or unsound mind, the tax liability is paid by there representative. That representative is also known as “Deemed Assessee”.

Here you can read:

HUF

HUF stands for “Hindu Undivided Family”.

But the main part is the term “HUF” has not been defined in the Income Tax Act 1961.

So, from where you can get the information about it?

From the Hindu Law.

According to that law, the HUF is consists of all persons lineally descended from a common ancestor and includes their wives and unmarried daughter.

HUF is a separate unit under the eyes of the law and distinct from its members.

The main person i.e. senior-most person is known as “Karta”.

Company

A company may be a Public or Private. It may be a domestic company or a foreign company.

Firm

Here firm means a partnership firm.

A partnership firm comes into existence by a partnership agreement between two or more persons.

LLP (Limited Liability Partnership) also comes under this category.

AOP and BOI

AOP means two or more persons joining together for a common purpose to earn income. It may also be noted that in the case of AOP there is no such intention to form a partnership.

Now you can see the term “Association of Persons”.

It means any person can form AOP.

Therefore any non-individual can also form AOP.

A person in AOP may be an individual or a company or a firm.

On the other hand, the term “Body of Individual” i.e. BOI shows that only individuals can form a BOI.

No non-individual can form a BOI.

However, intentions are common.

Both are formed for a particular objective and for earning money.

Local Authority

The Central Govt. or a State Govt. can not go to each and every area for administrative purposes.

For this reason, a local authority is formed.

A Local Authority is an organization that has the responsibility to provide all the services to common people of a particular area.

For example:

- Municipality.

- Corporation.

- Gram Panchayat.

- Cantonment Board.

Artificial Juridical Person

It is a really interesting one.

If somebody asks you is University a person?

The answer will be “Yes”.

But how?

A University is not an individual, not a HUF or a Company or a Firm.

Neither AOP nor a BOI.

Even it is not a Local Authority.

Then how can it be a person?

It is an Artificial Juridical Person not falling any of the above-mentioned persons.

It includes an idol or deity or a charitable institution, etc.

Every Assessee is a Person but every person is not an assessee.

It is a very important one.

An assessee is a person who is liable to pay the tax, either for his own income or in respect of others.

But it does not necessarily mean that every person is liable to pay tax.

If you are an individual and your total income is below the prescribed limit as per income tax slab.

Then you are not liable to pay tax.

If your income is nil then you are not liable to file return also.

In that case, you are not an assessee.

But you are a person.

So, it can be said that every assessee is a person but every person is not an assessee.

For your knowledge: Meaning of Assessee u/s 2(7) of the Income Tax Act 1961.

Example of Persons

Determine the status of the following:

a) Mr. Avishek. A Govt. employee

b) Mr. Narendra. A partner of a firm.

c) XYZ PVT. Ltd.

d) Mukherjee Biswas and Co.

e) Asansol Municipal Corporation.

f) The University of Burdwan.

Now let’s decide the status:

a) An Individual.

b) An Individual.

c) A Company.

d) A Firm.

e) A Local Authority.

f) An Artificial Juridical Person.

Final Word

I hope you have a proper idea about the term Person u/s 2(31) of the Income Tax Act 1961.

In case of any questions, feel free to ask me.

I am waiting for your comment.

Ok. Let’s end our discussion.

Meet you soon.

Ta-Da.

1 thought on “Definition of Person u/s 2(31) of Income Tax Act 1961”